Non Traditional Mortgage Definition

:max_bytes(150000):strip_icc()/GettyImages-155420417-0636da199f484064a9ac1e7af2b84012.jpg)

Nontraditional Mortgage Definition

Definition Of Qualified Mortgage 40 Year Mortgage Conventional Mortgage Mortgage Loan Officer

Advantages And Disadvantages Of Equitable Mortgage Mortgage Advantage Economical

Traditional And Non Traditional Functions Of Bangladesh Bank Bangladesh Function Traditional

Interest Only Mortgage Definition Interest Only Mortgage Interest Only Loan Mortgage

Traditional Investments Vs Airbnb Investments Infographic Investing Rental Property Investment Real Estate Infographic

The guidance offers a more narrow definition of nontraditional mortgage product which includes loans that have interest only and payment option terms described as adjustable rate mortgages arms where a borrower has.

Non traditional mortgage definition. So what is it that makes a loan non traditional this language actually refers to the lender from whom you procure the loan. A traditional mortgage would require a relatively high initial down payment of about 25 and 25. However recent economic conditions have spurred change in the business lending industry. Any mortgage loan not conforming to traditional and required lending guidelines could be considered a non conventional mortgage.

These expenses are tax deductible if they are business or work related. The definition as it appears in the guidance on nontraditional mortgage product risks is not as broad. A non conventional loan or mortgage is a type of loan that does not have to follow traditional mortgage loan requirements. They may pose even greater risk when granted to borrowers with undocumented or undemonstrated repayment capacity e g low or no documentation loans or credit characteristics that would be characterized as.

Examples of nontraditional mortgages can include mortgages that are interest only or subprime mortgages. Any travel expenses incurred while at a business convention. On top of that those with non traditional income such freelancers and business owners might have a better shot at funding with online mortgage lenders. Nontraditional residential mortgages exhibit characteristics that may result in increased risk relative to traditional mortgage products.

A broad term describing mortgages that do not take the traditional form. Nontraditional mortgage product according to 12 uscs 5102 6 the term nontraditional mortgage product means any mortgage product other than a 30 year fixed rate mortgage legal definition list. Yates points out that non traditional mortgage lenders are more willing to take a risk on those with lower credit scores. In the past banks were the primary entities who granted these types of arrangements.

Conventional Loan Rates And Requirements For 2020 Mortgage Rates Mortgage News And Strategy The Mortgage Reports

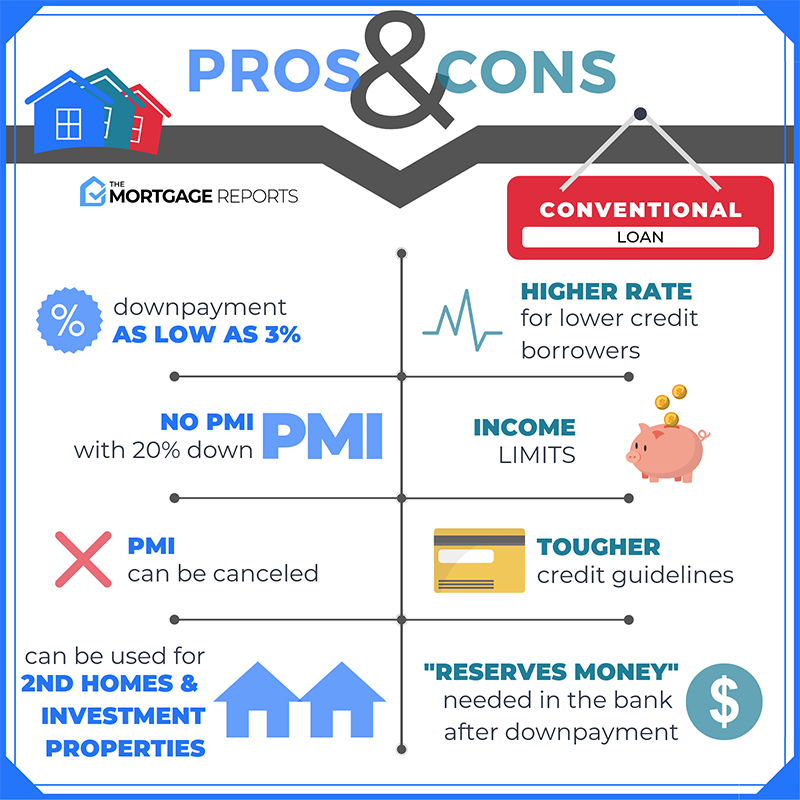

Difference Between Conventional And Non Conventional Mortgages

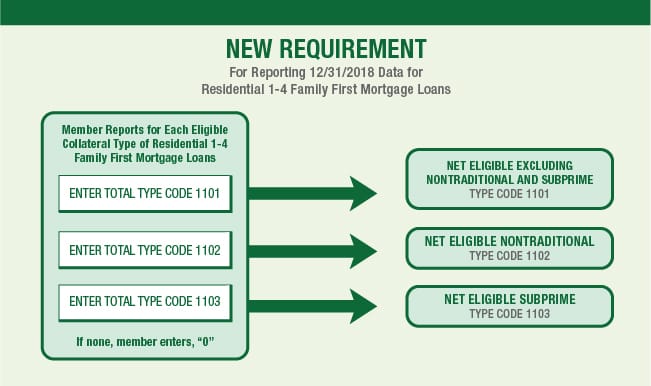

2019 New Collateral Definitions And Reporting Requirements Fhlb Des Moines

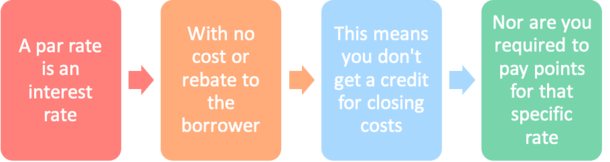

What Is The Par Rate The Truth About Mortgage Com

Loan Vs Mortgage Difference And Comparison Diffen

Home Business Ideas In Germany Save Real Estate Investing Business Books Against Home Business Insurance Real Estate Investing Learn Accounting Business Books

Financial Ratio Cards Financial Ratio Accounting Basics Financial

Please Contact Me For Your Next Real Estate Transaction Jody Saunders Licensed Real Estate Salesperso Mortgage Marketing Real Estate Salesperson Real Estate

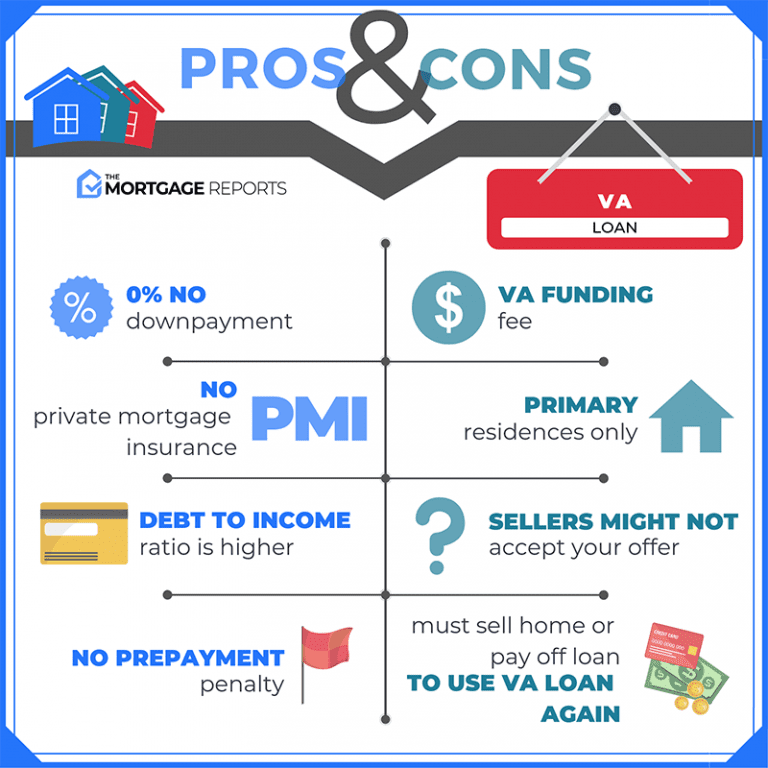

10 Biggest Benefits Of Va Home Loans In 2020

Mortgage Quality Control Plan Template Inspirational Process Audit Checklist Temp In 2020 Mission Statement Template Business Plan Template Free Business Plan Template

Get Instant Business Loans From Mobile App At Play Store Lendingkart Lending Art Finance Limited Is A Non Deposit Small Business Loans Business Loans Loan

Https People Lend In Loan Lending P2p Lending The Borrowers

But First Get Pre Approved Realtor Quote Loan Officer Quote Realtor Office Decor Loan Office Real Estate Quotes Real Estate Office Estate Agent Office

Pin By Shadia Ghreayeb On Aes Elegance Gowns Nice Dresses Green Wedding Dresses

Fabric Application Flow Example Blockchain Fabric Fintech

Are You Setting Goals The Right Way Budgeting Budgeting Finances Saving Money Budget

Earn A Referral Fee We Buy Houses Referrals Real Estate Investor

Roth Ira Vs Roth 401 K Simplefinancialfreedom Com Finance Investing Retirement Savings Plan Finance

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gct8kttzm7dxcgf6jzp Ns9cfzv3g5vi5wbgo1nkffk Usqp Cau

Difference Between Online Offline Share Trading Angel Broking Online Trading Online Share Trading

Pin Pa Mortgage

Transfer Of Business Ownership Agreement Template Best Of Payment Contract Templates Contract Template Receipt Template Legal Forms

Pin On Wealth Creation

Startups Reshaping Residential Real Estate Buying And Selling Residential Real Estate Real Estate Tech Startups

Financial Samurai Passive Income 2017 Passive Income Financial Income

Real Estate Math Exam Prep Course Real Estate Exam Maths Exam Real Estate Courses

Executive Roadmap To Fraud Prevention And Internal Control Creating A Culture Of Compliance Ebook Rental Internal Control Credit Repair How To Fix Credit

A Non Deductible Ira Is A Retirement Account That Behaves Like A Traditional Ira Except That It Is F Retirement Planning Huntington Beach California Deduction

A Very Comprehensive Rent Vs Buy Calculator Doncaster Mortgage Estate Agency

Zero Based Vs Traditional Budgeting Budgeting Base Traditional

Pin On Buying Investment Property

Goodwill Classes Cat Dog Rat Rabbit Valuation Factors Affecting Bookkeeping Business Financial Accounting Accounting And Finance

Google Releases Penguin 3 Penguins Google Release

Advantages And Disadvantages Of Life Insurance Policy Life Insurance Policy Insurance Policy Life Insurance

Loan Level Pricing Adjustments Llpa A Complete Guide

A Simple Business Plan Small Business Plan Small Business Plan Template Simple Business Plan

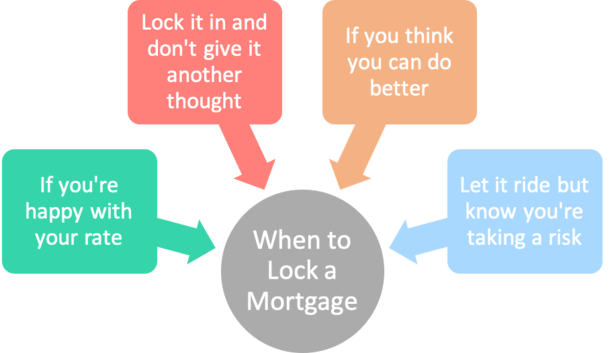

Mortgage Rate Lock Always Lock Your Mortgage The Truth About Mortgage Com

Fixed Rate Vs Adjustable Rate Mortgages

Major Roles And Responsibilities Of The Business Analyst Business Analyst Business Analyst Career Business Analysis

Pin Auf Website Traffic

Chart Of Accounts Template Unusual How To Use The Same Chart Account Structure For A New Of 37 Inc Chart Of Accounts Accounting Templates Free Design

Have A Bad Credit And Unable To Secure A Business Loan Get Your Credit Score Back On Track With Bad Credit With Images Business Loans Improve Your Credit Score Bad Credit